New GST Slabs 2026: Simplify Your Tax Compliance & Calculations

Table of Contents

GST 2.0 Decoded: Navigating the 2025–26 Two-Tier Slabs and New Calculation Rules

Master the GST 2.0 reform with our expert guide to the new two-tier tax slabs. Learn how to calculate your GST accurately and streamline your business compliance.

India's tax framework entered a new era on 09/22/2025, and understanding the new GST rates 2025 is now a baseline requirement for every business owner, finance professional, and consumer operating in this environment. GST 2.0 — the most significant restructuring of the Goods and Services Tax since its 2017 introduction — dismantles the old four-tier slab system and replaces it with a streamlined framework built around three active rates: 5%, 18%, and 40%. The result is a structure designed to reduce classification disputes, lower compliance costs, and deliver measurable relief on everyday goods.

This guide decodes every layer of that transformation. You'll find a precise breakdown of which slab covers which goods and services, step-by-step calculation formulas updated for the 2025–26 filing cycle, and a clear-eyed analysis of how these changes affect retail pricing, business margins, and input tax credit strategy. Whether you're reconfiguring your ERP system, updating invoice templates, or simply trying to understand what you're paying at checkout, the sections ahead give you the complete picture — no guesswork required.

The GST 2.0 Revolution: Why the 2025–26 Overhaul Changes Everything

Learning New GST Rates 2025 doesn't have to be complicated. India's tax landscape shifted permanently on 09/22/2025. GST 2.0 Reform — the most consequential restructuring of the Goods and Services Tax since its landmark 2017 rollout — eliminated the long-criticized four-tier slab system and replaced it with a cleaner, more intuitive framework designed to reduce compliance friction and stimulate consumer spending.

GST 2.0: The sweeping overhaul of India's Goods and Services Tax structure, effective September 22, 2025, consolidating the previous 5%, 12%, 18%, and 28% primary slabs into a streamlined two-tier system anchored at 5% and 18%.

Key Date: 09/22/2025 — The date the New GST Rate Structure officially took effect, replacing every rate card, ERP configuration, and invoice template your business depends on.

The End of the 12% and 28% Slabs

According to ClearTax, the GST Council overhauled the previous four-tier system into a primary structure of just 5% and 18%. The 12% slab — which covered hundreds of everyday goods — has been sunsetted entirely. Critically, approximately 99% of items previously taxed at 12% migrate downward to the 5% slab, delivering direct cost relief to businesses and end consumers alike.

The 28% slab, historically the most contentious bracket, is also being restructured. Luxury and so-called "sin goods" previously taxed at 28% plus a cess are transitioning to a new de-merit category — but that's a conversation for the next section.

Why Simplification Drives Growth

The core thesis behind New GST Rates 2025 is straightforward: fewer brackets mean lower compliance costs, faster filing, and reduced classification disputes. When compliance becomes less burdensome, businesses reinvest savings into volume — and volume drives consumption. According to government data, this reform is explicitly positioned as relief for common consumers and a growth catalyst for businesses.

Understanding which goods land in which slab — and why — is the critical first step every finance team, e-commerce operator, and retailer must take before the next filing cycle.

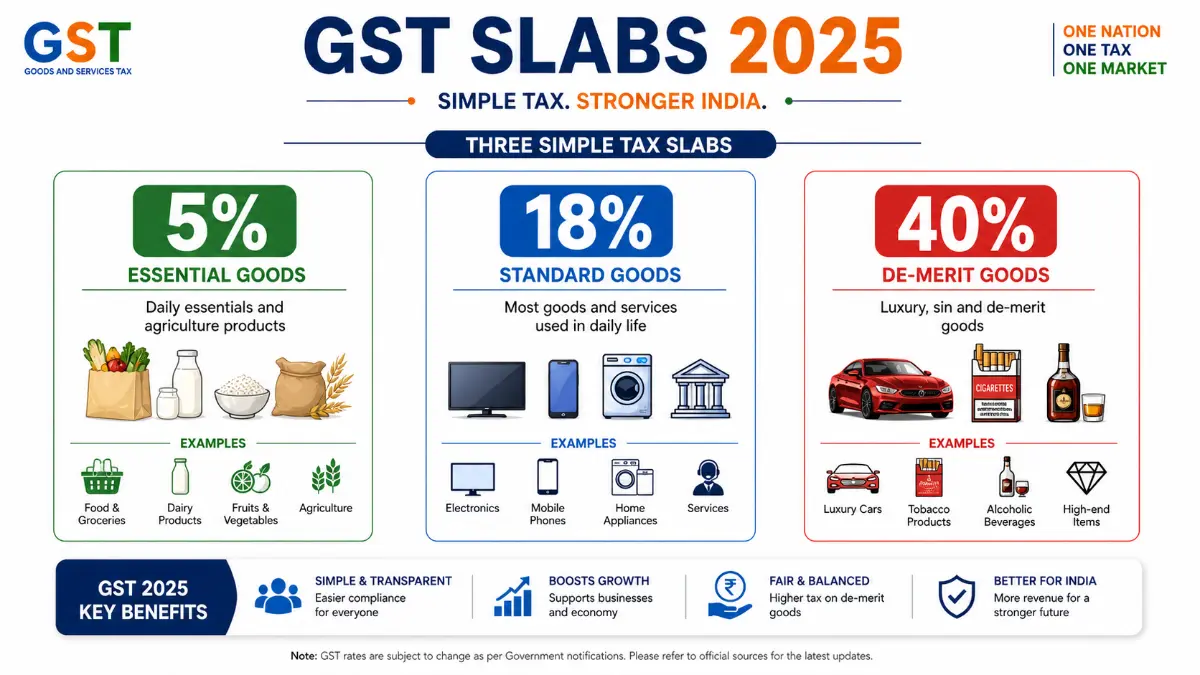

The New GST Slab Structure for 2025–26: 5%, 18%, and 40% Explained

The GST 2.0 overhaul didn't just shuffle numbers — it fundamentally rewired the logic of how goods and services are categorized. Understanding the GST Slabs 2025-26 is no longer optional for business owners, finance professionals, or informed consumers. The old four-slab model (5%, 12%, 18%, 28%) has been compressed into a cleaner three-tier system, and knowing exactly where your products or services land can mean the difference between accurate compliance and costly penalties.

Here's a definitive breakdown of each active tier.

The 5% Essential Tier

Essential Tier: The lowest active GST rate, reserved for goods that support basic consumption needs — including many items previously taxed at 12%.

The 5% slab is now significantly broader than before. According to Tally Solutions, approximately 99% of items that previously sat in the 12% category were moved into the 5% bracket under GST 2.0. That's a meaningful reduction in the tax burden on everyday goods.

Items now falling under the 5% Essential Tier include:

- Processed and packaged foods (certain branded snacks, dairy products, and edible oils)

- Basic kitchenware and cookware items previously at 12%

- Pharmaceutical inputs and select medical equipment

- Agricultural goods that undergo minimal processing

- Public transport services and economy-class air travel

For households managing tight budgets, this consolidation translates directly into lower out-of-pocket costs on routine purchases.

The 18% Standard Tier

The 18% slab functions as the workhorse of the GST structure — broad, predictable, and applicable to the majority of manufactured goods and commercial services. Kotak Mutual Fund's GST 2.0 overview confirms that roughly 90% of items previously in the 28% slab were reduced to 18%, making this tier the new center of gravity for mid-range goods.

Categories firmly within the 18% Standard Tier include:

- Consumer durables such as washing machines, refrigerators, and air conditioners

- Most financial and professional services

- Telecom services and broadband connectivity

- Paints, adhesives, and construction materials (standard grade)

- Restaurant services at non-air-conditioned venues

- Software products and IT-enabled services

The 18% slab now represents the baseline expectation for most business-to-business transactions — a fact that simplifies input tax credit calculations considerably.

The 40% De-merit Tier

De-merit Goods: Products where government policy deliberately uses tax to discourage consumption, typically covering luxury items, tobacco, and environmentally harmful goods.

The old 28% rate plus a variable compensation cess has been replaced by a flat 40% GST slab, creating far greater pricing predictability for businesses in these categories. This consolidation eliminates the administrative complexity of calculating cess separately.

Goods currently classified in the 40% De-merit Tier include:

- Luxury automobiles (premium sedans, SUVs above defined price thresholds)

- Aerated beverages and energy drinks

- Tobacco products and pan masala

- High-end consumer electronics positioned as status goods

- Casinos, betting, and online gaming platforms

The flat 40% structure makes compliance more straightforward — but the effective tax burden on end consumers in these categories is substantial.

Nil-Rated and Exempt: What Stays at 0%

Not everything carries a GST rate. Nil-rated goods are formally listed in the GST schedule at 0%, while exempt supplies fall outside the taxable scope entirely. Fresh vegetables, unprocessed grains, milk, eggs, and essential healthcare services remain at zero cost to the consumer from a GST standpoint.

One important caveat: businesses supplying exclusively nil-rated or exempt goods cannot claim input tax credit on their purchases — a structural trade-off worth factoring into pricing models.

The architecture of these three tiers sets the stage for a critical question: which specific products migrated between slabs, and what does that mean for your monthly spending? That's precisely what the next section unpacks in detail.

Deep Dive: The Great Migration of Goods and Services

So what are the new GST slabs for 2025, and which specific products actually moved? The restructured rate architecture affects thousands of line items — but a handful of category shifts carry outsized significance for everyday Indian consumers and business owners alike. Understanding which goods migrated, and why, reveals the deeper policy logic driving GST 2.0.

From 12% to 5%: Everyday Relief That Adds Up

The most immediately felt shift is the downward migration of essential and near-essential goods from the old 12% tier into the new 5% slab. Processed foods — including packaged namkeen, ready-to-eat meals, and branded spices — now attract just 5% GST. Specific kitchenware categories, including pressure cookers and basic cookware, also made this transition. Personal hygiene products and certain pharmaceutical inputs followed a similar path.

| Item Category | Old Rate | New 2025 Rate | Impact |

|---|---|---|---|

| Packaged processed foods | 12% | 5% | Lower shelf prices for middle-income households |

| Basic cookware & kitchenware | 12% | 5% | Reduced cost on routine household purchases |

| Certain personal hygiene goods | 12% | 5% | Direct savings on monthly spend |

| Consumer durables (ACs, washing machines) | 28% | 18% | Significant price relief on big-ticket purchases |

| Premium automobiles | 28% + Cess | 40% (flat) | Simplified but elevated rate for luxury segment |

| Aerated drinks & tobacco products | 28% + Cess | 40% (flat) | De-merit consolidation; no structural relief |

The GST 2.0 Guide from Unicommerce confirms that these downward shifts are designed to reduce the compliance burden for fast-moving consumer goods sellers, not just lower end prices. Fewer rate brackets mean fewer misclassification risks on invoices — a practical win for both retailers and their customers.

From 28% to 18%: The Consumer Durables Dividend

The drop from 28% to 18% on consumer durables deserves particular attention because it directly changes the math on middle-class aspirational spending. Air conditioners, washing machines, refrigerators, and large-screen televisions all fall into this reclassified tier. On a $600 appliance purchase, that 10-percentage-point reduction translates to roughly $60 in tax savings — meaningful when multiplied across a household's upgrade cycle.

The compounding logic here is significant: lower rates tend to pull forward demand from consumers who were previously on the fence. The Economic Survey 2025–26 (via Upstox) notes that "volume effects could offset the impact of rate reductions on revenues" — meaning the government is wagering that higher consumption will compensate for thinner per-unit tax collections. In practice, this bet tends to pay off in categories where price sensitivity is high and purchase decisions have been deferred.

The 'De-Merit' Logic: Why 40% Is Its Own Category

De-merit goods: Products the government actively discourages through elevated taxation — typically luxury items, harmful consumables, or goods associated with negative social externalities.

Premium cars, aerated beverages, and tobacco products now sit in a consolidated 40% flat slab. Previously, these attracted a 28% rate plus a separate Compensation Cess, creating calculation complexity and frequent litigation over cess applicability. The 40% flat structure eliminates that ambiguity — the rate is punitive by design, not by accident. This is a clear policy signal: the government isn't just taxing these goods, it's structurally discouraging their consumption relative to the lower tiers.

The 2026 Transition Outlook

Several product categories remain in a formal review period under the GST Council's 2026 roadmap. Textile intermediates, certain construction materials, and health supplements are flagged for potential reclassification as compliance data from the post-09/22/2025 period matures. Businesses operating in these categories should monitor GST Council notifications closely — a further downward revision to 5% for some construction inputs remains a live possibility.

Knowing where items now sit is only half the equation. The next step is calculating exactly how much tax applies — and the formulas for the 5%, 18%, and 40% slabs each carry their own nuances worth mastering.

How to Calculate GST in 2025–26: Step-by-Step Formulas

Now that you understand which goods and services moved to which slab, the practical question becomes: how do you actually run the numbers? The GST rate changes 2025-26 didn't just shift percentages — they also introduced a brand-new 40% tier that calculates differently from the old cess-based structure. Getting the math right from the start saves costly reconciliation headaches later.

The Core Formula (All Slabs)

The foundational calculation hasn't changed, but applying it correctly across three distinct rates now matters more than ever.

The Basic GST Formula:

GST Amount = (Original Cost × GST Rate) / 100 Final Price = Original Cost + GST Amount

This formula applies uniformly across the 5%, 18%, and 40% slabs. What changes is how the resulting GST amount gets split between central and state authorities — and that split determines your actual tax liability on every invoice.

Calculation Example — 5% Slab (Intra-State)

Item: Packaged buttermilk | Base Price: $50

- GST Amount = ($50 × 5) / 100 = $2.50

- CGST (2.5%) = $1.25

- SGST (2.5%) = $1.25

- Final Invoice Value: $52.50

For an inter-state transaction, IGST replaces the CGST + SGST split: IGST = $2.50 (full 5%), billed as a single line item.

Calculation Example — 18% Slab (Intra-State)

Item: Business software license | Base Price: $200

- GST Amount = ($200 × 18) / 100 = $36.00

- CGST (9%) = $18.00

- SGST (9%) = $18.00

- Final Invoice Value: $236.00

Inter-state equivalent: IGST = $36.00 (full 18%) as a single charge.

Calculating for the 40% Slab: What's Different

The 40% tier is structurally distinct from the pre-2025 cess model. Under the old framework, sin goods carried a 28% base rate plus a separate GST Compensation Cess — two line items on every invoice. The new 40% slab consolidates everything into a single unified rate. There are no layered cess calculations to reconcile.

GST Compensation Cess: A surcharge levied on top of the base GST rate on select luxury and demerit goods, historically used to compensate states for revenue losses during GST rollout.

One important caveat: according to Bajaj Finserv, tobacco products remain at 28% plus cess until state compensation loan obligations are fully discharged, despite being slated for the 40% slab. In practice, this means businesses dealing in tobacco must still calculate two separate charges — the base rate and the cess — rather than applying a flat 40%.

CGST, SGST, and IGST Split Rules

The split logic is straightforward but non-negotiable:

- Intra-state supply: Total GST splits equally — half to CGST, half to SGST

- Inter-state supply: Full GST charged as IGST (collected by the central government, later apportioned to destination state)

- Union Territories: UTGST replaces SGST for intra-UT transactions

Reverse Charge Mechanism (RCM) Updates for 2025–26

Reverse Charge Mechanism (RCM): A GST provision where the recipient of goods or services — rather than the supplier — is liable to pay tax directly to the government.

The 2025–26 reforms expanded RCM applicability, particularly for unregistered suppliers transacting with registered businesses. Under updated GST return filing guidelines, recipients under RCM must self-invoice, pay the applicable slab rate (5%, 18%, or 40%), and report the liability in their GSTR-3B filing — input tax credit on RCM payments remains claimable in the same return period, provided the transaction qualifies.

Understanding the math is only one dimension of GST 2.0 compliance. The more significant question for businesses and consumers alike is what these restructured slabs actually do to prices, margins, and economic behavior at scale — which is exactly what the next section examines.

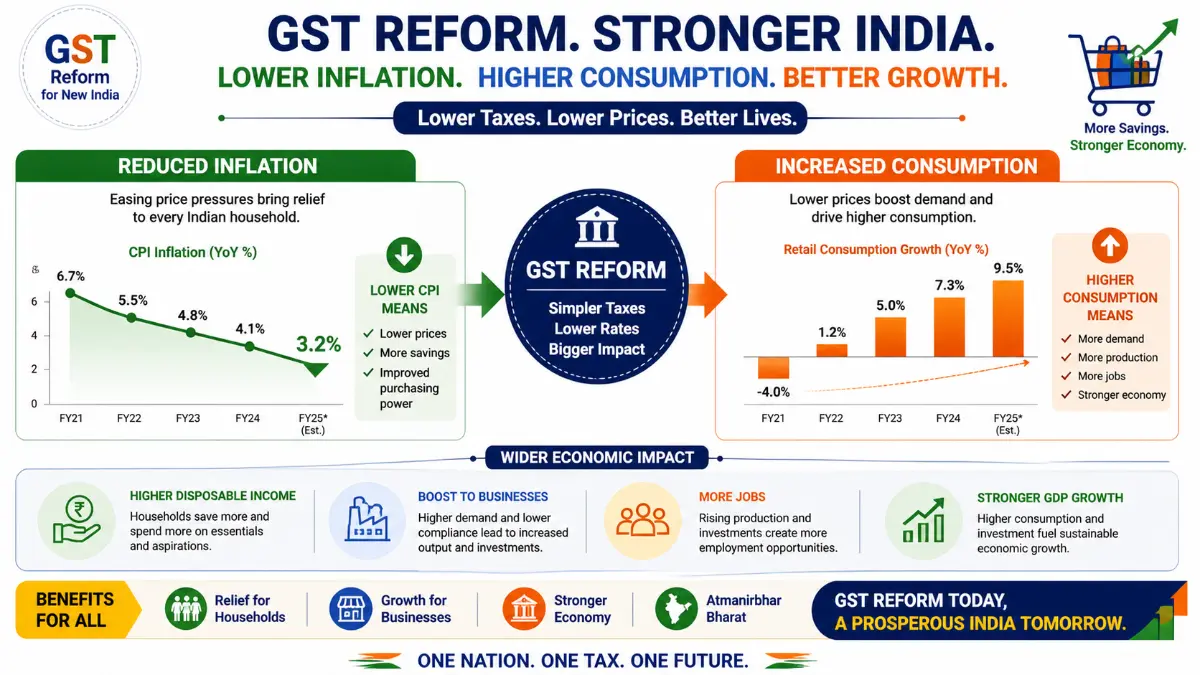

Economic Impact: Inflation, Consumption, and Your Bottom Line

Understanding how to calculate GST for 2025–26 is only half the equation. The other half is grasping what these structural changes actually do to prices, profits, and the broader economy. Rate rationalization is not a cosmetic exercise — it reshapes consumer behavior, business strategy, and long-term tax compliance in measurable ways.

Retail Inflation: A Real Reduction in the Cost of Living

The most immediate effect of GST 2.0 is felt at the cash register. According to SBI Research, the sweeping rate rationalization implemented in late 2025 is estimated to reduce the Consumer Price Index (CPI) by approximately 25 to 35 basis points for the 2025–26 fiscal year.

Basis Point (bps): One basis point equals one-hundredth of a percentage point (0.01%). A 25–35 bps reduction in CPI translates to a tangible, if modest, increase in household purchasing power across income brackets.

For everyday consumers, this means products that previously attracted a 12% rate — now consolidated into the 5% or 18% bands — arrive slightly cheaper. Essentials shift downward; luxury and de-merit goods carry the 40% load. The net effect is a more progressive tax burden, where lower-income households benefit disproportionately from rate cuts on common goods.

Stat callout: A 25–35 bps drop in CPI may sound small, but at scale across a $3.5 trillion economy, it represents billions of dollars in restored purchasing power flowing back to consumers annually.

Business Margins: The Volume Play in Action

Lower tax rates do not automatically shrink profit margins — and for many businesses, the reverse is true. When prices fall, price elasticity of demand kicks in: consumers buy more, transaction volumes rise, and businesses that previously operated informally or under-declared sales find it economically rational to participate fully in the formal economy.

In practice, a mid-sized manufacturer facing reduced GST liability on finished goods can price more competitively, capture market share, and drive revenue growth through volume rather than margin compression. The elimination of the 12% slab also removes a persistent classification dispute that tied up working capital in litigation — freeing cash for operations instead.

Compliance Benefits: Shrinking the Shadow Economy

Tax simplification — reducing the number of active slabs from four to three — directly correlates with improved voluntary compliance. Fewer rate categories mean fewer misclassification opportunities, less ambiguity during audits, and a reduced incentive for the informal sector to stay off the books.

The GST 2.0 Reforms are designed with this explicit goal: broaden the tax base rather than squeeze existing taxpayers harder. Historically, complexity itself was a driver of the shadow economy. Businesses avoided registration simply because navigating four overlapping slabs, contested HSN code mappings, and cascading litigation was more costly than staying invisible. A streamlined two-tier structure changes that calculus.

The 2026 Outlook: Structural Stability Ahead

Policy signals strongly suggest the two-tier architecture — anchored at 5% and 18%, with a 40% ceiling on de-merit goods — is designed for medium-term stability. Rate fatigue has been a persistent complaint from industry; frequent revisions disrupted pricing models and ERP configurations quarter after quarter. The current framework appears intentionally durable, giving businesses a reliable foundation for multi-year planning.

That stability, however, brings its own set of operational demands — from updating accounting systems to retraining billing teams — which is exactly where the next section picks up.

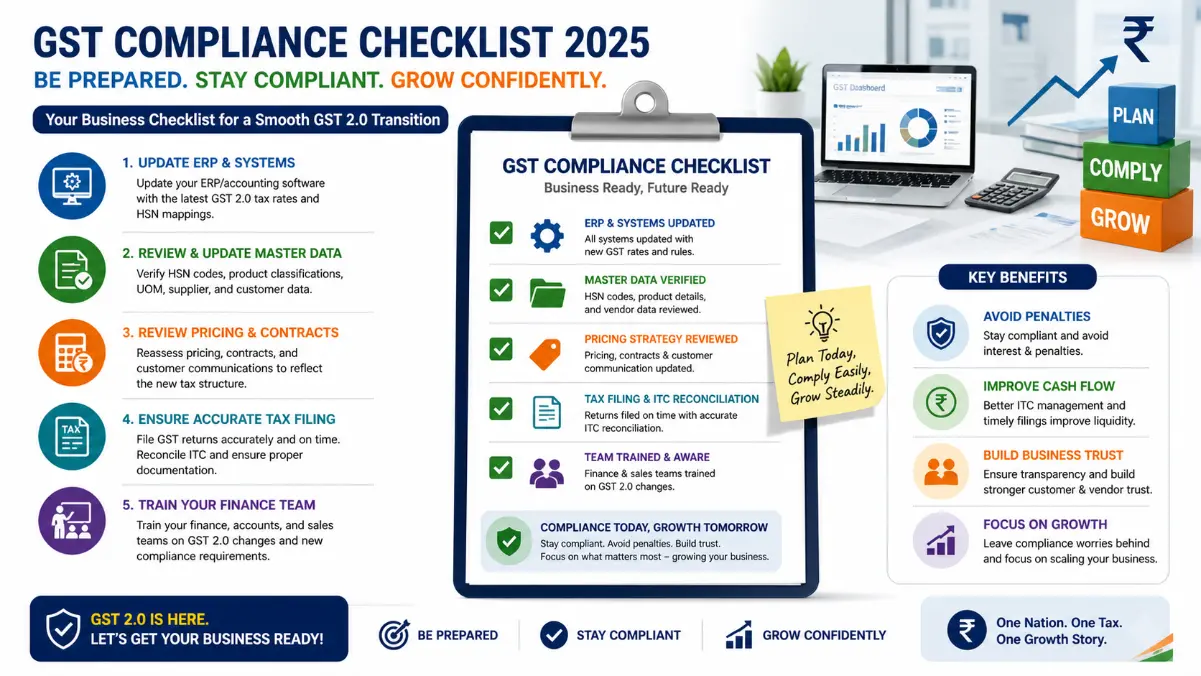

Compliance Checklist: Preparing Your Business for GST 2.0

With the September 22, 2025, effective date now live, businesses operating under the revised gst rates in india 2026 framework must move from awareness to action. Proactive compliance isn't just about avoiding penalties — it's about protecting margins and maintaining customer trust.

- Update ERP and Accounting Software

Map every product and service to its revised HSN code before processing a single invoice under the new structure. The shift from a four-slab model to a streamlined three-slab system (5%, 18%, and 40%) means legacy tax codes in your software are likely misaligned. A miscoded product can trigger audit flags and cascading ITC errors downstream.

- Review Your Pricing Strategy

Anti-profiteering provisions require businesses to pass on rate reductions to end consumers. If a product moved from 12% to 5%, your invoice price should reflect that benefit — documented clearly. Failure to adjust pricing while retaining the tax savings is a compliance risk, not just an ethical one. Review price lists and update customer-facing documents accordingly.

- Reconcile Existing ITC Balances

Credits accumulated under the old 12% and 28% slabs don't automatically realign. Work with your finance team to audit the ITC ledger, identify credits tied to reclassified categories, and confirm correct carryforward treatment under the updated GST return filing rules. Errors here compound quickly across quarterly filings.

- Train Your Billing and Finance Teams

The new 40% de-merit slab — covering aerated drinks, premium cars, yachts, and private aircraft — replaces the previous 28% plus cess structure. Billing teams must clearly distinguish this top-tier rate from the standard 18% rate to avoid under-collection or overcharging. A short internal training session with documented reference sheets goes a long way.

The businesses that treat GST 2.0 as an operational upgrade — not just a regulatory change — will find themselves better positioned for the compliance landscape ahead.

Start your checklist today, and build systems that make the next reform cycle far less disruptive.

Key New Gst Rates 2025 Takeaways

- The GST 2.0 Revolution: Why the 2025–26 Overhaul Changes Everything

- The New GST Slab Structure for 2025–26: 5%, 18%, and 40% Explained

- Deep Dive: The Great Migration of Goods and Services

- How to Calculate GST in 2025–26: Step-by-Step Formulas

- Economic Impact: Inflation, Consumption, and Your Bottom Line

Generated by Frase

Related articles

Keep reading similar topics

Precision Word Counter: Accurate Character & Word Count Tool

Need an accurate word count? Use our professional word counter tool to ensure your writing meets strict length requirements for publishing, SEO, and more.

The Truth Behind DOB Calculators: Why They Go Viral

Ever wonder why birth date calculators are so addictive? Discover the psychology behind viral DOB trends, astrology charts, and the secrets hidden in your birth.

Why the Best Online Word Counter Is Your Ultimate Writing Tool

Stop using basic calculators. Discover why a professional word count checker is an essential writing assistant for precision, clarity, and better content.